Radiopharmaceutical supply chain structure: 1/6

Step 1 – Source material acquisition: is raw material supply a real threat to nuclear medicine?

Prior to the enrichment stage, the industry needs to secure various ores (Nickel, Tellurium, Yttrium, Zinc, etc.). With the booming demand for medical radionuclides, a critical question arises: are we facing a major supply chain risk for our starting materials?

The short answer: It depends on whether we are talking about stable isotopes or radioactive source materials. Here is a quick breakdown 👇

✅ Stable isotopes / rare earths: a manageable risk

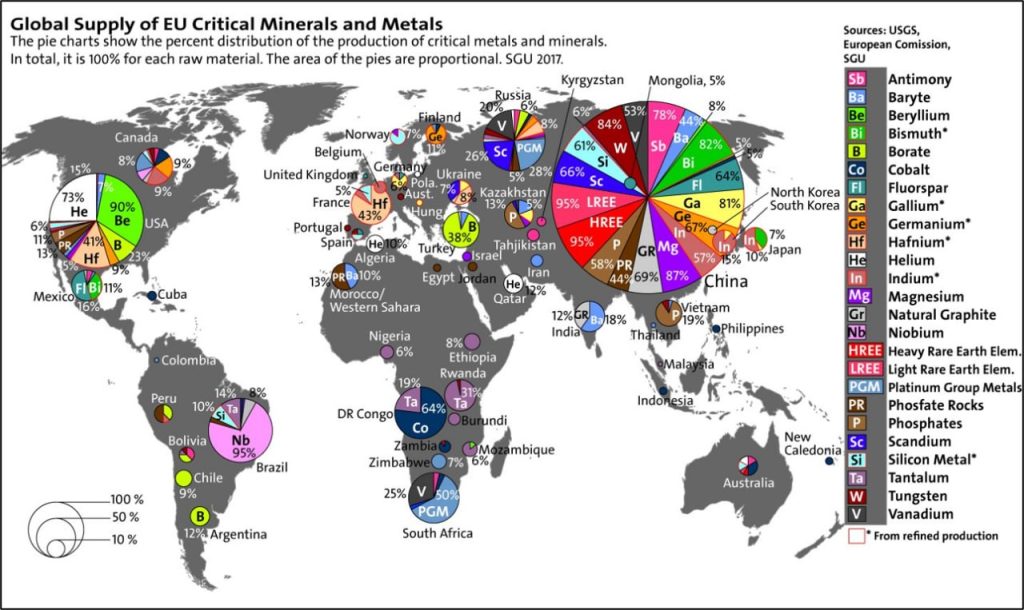

While rare earths can be a massive geopolitical vulnerability for electric vehicles, IT, or wind turbines (as seen in attached figure showing critical raw materials supply), the story is different for nuclear medicine. Because the quantities required for medical applications are so small, the risk is highly manageable. In a worst-case scenario, building strategic stockpiles for medical use could be entirely feasible.

⁉️ Radioactive source materials: a potential bottleneck?

This is where sourcing generally gets complex, expensive, and highly specific:

– Uranium: Directly sourced and enriched for nuclear power use, but securing enrichment up to 20% in metallic form for medical targets remains a challenge (to be discussed next week 😊)

– Thorium-232: Historically a waste product of uranium mining, it is now becoming crucial for Lead-212 production. Major players like Orano Med have already heavily invested in processing existing Thorium stocks.

– Radium-226: The essential precursor for Actinium-225. There is no active mining for Radium today. While some players (like PANTERA) have access to significant historical reserves, mining companies could be hesitant to invest in new extraction facilities for a market that is still defining itself.

💡 The Takeaway

On the MEDraysintell side, apart from radioactive materials, raw source material supply generally does not raise major concerns; small quantities can still be easily secured on the international market. The real challenge could lie in some specific material for which no ore market exists.

With the demand for radionuclides set to rise, amid geopolitical tensions and export restrictions of rare earths, could raw material supply become a cross-cutting risk for the industry? Or should we only anticipate market tightness for specific ores, such as Radium, where mining activities were suspended decades ago?

Figure source: USGS, European Commission, SGU (2017)