Radiopharmaceutical supply chain structure: 2/6

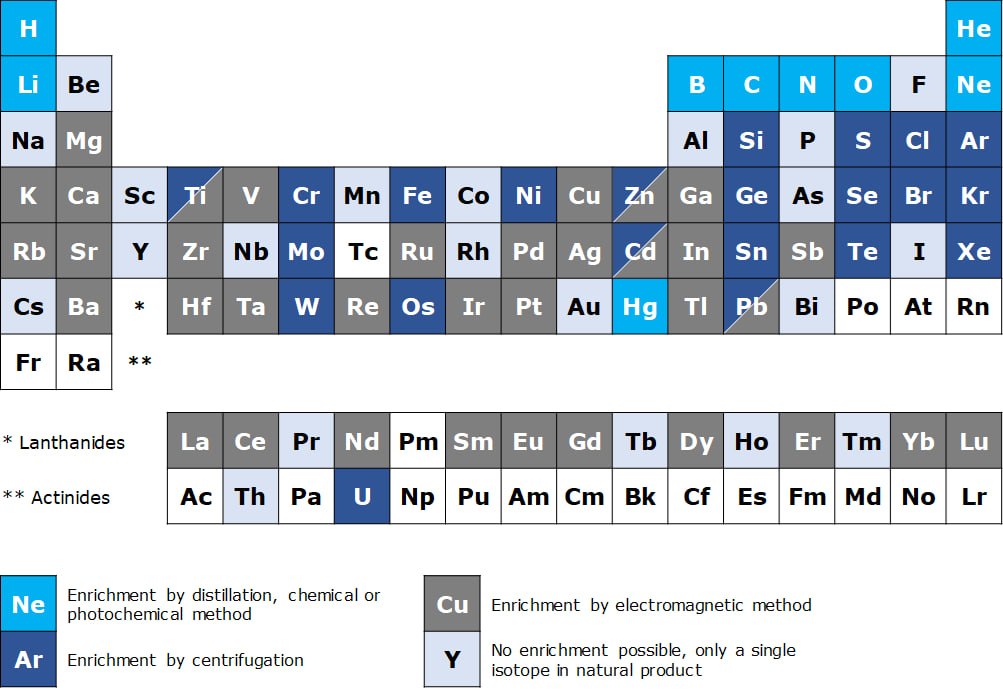

Step 2 – Isotope Enrichment

Creating materials for nuclear medicine is incredibly tough, and it all comes down to how “clean” the raw ingredients are. To illustrate that, let’s look at two contrasting examples: Holmium and Ytterbium.

🟢 Holmium: Natural Holmium is monoisotopic, meaning it consists of nearly 100% Holmium-165. We can put natural ore straight into a reactor to produce Holmium-166. There is no need for isotopic enrichment because there are no competing isotopes to get in the way. It’s a straight, efficient path from the earth to the reactor. Unfortunately, Holmium is the exception, not the rule. ⚠️

🔴 Ytterbium: Natural Ytterbium is a ‘noisy’ mixture of seven different isotopes. They range from 168Yb at a mere 0.12% abundance, up to 174Yb at 32%. But only 176Yb is of interest to us (as the precursor for Lutetium-177). If we irradiate natural Ytterbium, the reactor activates all those isotopes simultaneously. This creates a mix of unwanted side products that are chemically identical to our target, making them impossible to separate afterward. Because of this, we need ultra-pure Ytterbium-176, enriched to 99.9% or higher. And it costs a lot more than natural ore.

For enrichment, physics dictates the tool. Industry must match the technology to the isotope’s specific physical and chemical properties.

In the modern medical supply chain, we rely on three primary pillars:

– 🧪 Distillation: A mature market with strong international competition and low supply risk, but limited to light elements like 18O (used for 18F production).

– 🔄 Centrifugation: Dominated by strong industrial players (ECP JSC, Urenco Isotopes, and Orano) sharing a complex market. Production campaigns are only launched once demand hits an economic threshold, sometimes creating supply tension for low-demand isotopes.

– ⚡ Electromagnetic Separation (EMIS): A Russian monopoly (EKP JSC) for decades that is finally being challenged by new players (Kinectrics, TMC), heavily driven by the booming demand for 177Lu. This bottleneck should progressively disappear.

Beyond these three pillars, the ecosystem is rapidly evolving. We are seeing laser-enrichment developments (Orano, ASP Isotopes), versatile research facilities like the Enriched Stable Isotope Prototype Plant (ESIPP) and its follower SIPRC, and many other players experimenting with proprietary tools.

With such a renewed wave of interest and investment in the ecosystem, what do you think should be done next to further support these industrial developments? 👇

Image source : MEDraysintell/NucAdvisor